Fibre by Fibre: A Working Guide

Fibre is the starting point of every garment. It shapes the look, the feel, and the way a piece performs over time. Any sustainability choice begins at the design stage, and fibre is the first decision in that process

Look more closely at the label inside any garment. Two pieces of information consistently reach the consumer: the country of origin (the "Made In" line) and the fibre composition (100% cotton, 80% polyester 20% elastane, 70% viscose 30% linen). The fibre line is one of the most regulated pieces of information in fashion, but on its own it says very little. It does not tell you where the fibre came from, who handled it, or what processes were used to turn it into fabric.

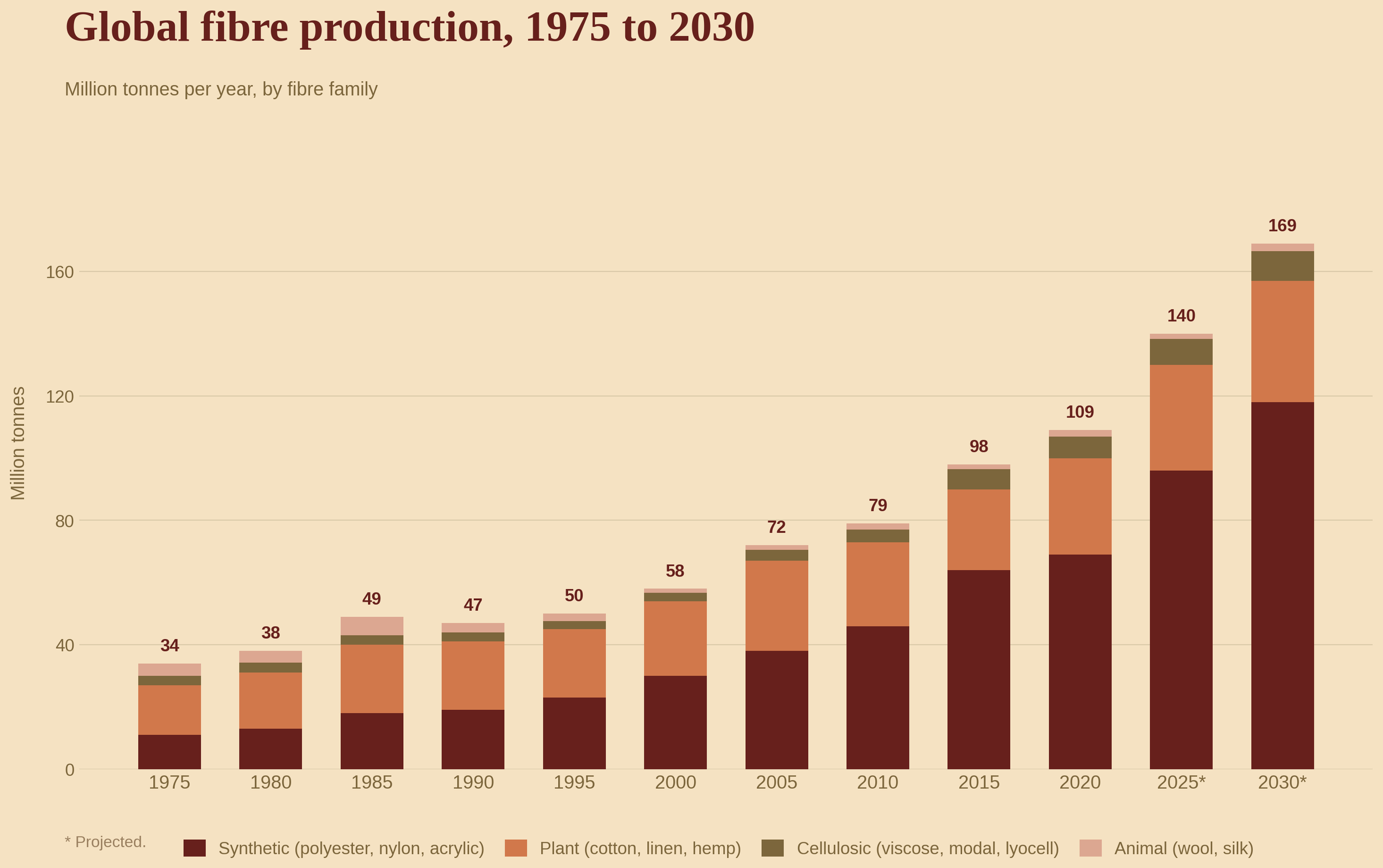

Global fibre production reached 132 million tonnes in 2024, more than double the figure for 2000. Polyester accounted for 59% of that total, cotton 19%, manmade cellulosics (viscose, modal, lyocell) 6%, other plant-based fibres around 5%, and animal fibres combined under 1%. 88% of polyester is still fossil-based, and 98% of "recycled" polyester is made from PET bottles rather than from textile waste.

Data: Textile Exchange, Materials Market Report 2025 (based on CIRFS, FAO, ICAC, IVC, IWTO, Maia Research). Synthetic includes polyester, polyamide (nylon), acrylic and other oil-derived fibres. Plant includes cotton, linen, hemp, jute and other plant fibres. Cellulosic (MMCF) includes viscose, modal and lyocell. Animal includes wool, silk and other animal fibres.

The shape of that chart is largely the story of polyester. Fibre production doubled between 2000 and 2024, polyester accounts for almost all of the growth. The synthetic boom is what made cheap, fast, year-round production possible at the volumes the modern fashion industry now runs on.

The eight fibres in this guide together represent roughly 95% of global fibre output. They fall into three families:

Natural (plant and animal): cotton, linen, wool, silk

Cellulosic: viscose, Tencel

Synthetic: polyester, recycled polyester

For each fibre: characteristics, the main risks, the certifications worth knowing, and wholesale price per linear metre.

Natural

-

% of global fibre: 19%, 24.5 million tonnes in 2024

Production countries: India, China, the United States, Brazil, Pakistan, Uzbekistan, Turkey

Benefits

A soft, breathable plant fibre that absorbs moisture well.

Takes dye cleanly across most colour palettes.

Works at every price point, from basic jersey to fine shirting.

Familiar to consumers and supported by mature mill infrastructure across all major producing countries.

Risks

Human & health

Forced labour has been documented in several major cotton-producing regions. Xinjiang is the most prominent recent example: around 20% of global cotton comes from there, and goods produced in the region are subject to import restrictions in the United States and growing scrutiny in the EU and UK

Smallholder cotton farmers in parts of India have been linked to long-running debt cycles around seed, irrigation, and crop failure, with chronic mental health and suicide rates significantly higher than the rural average

Spinning and ginning operations in South Asia have a documented history of bonded and exploitative labour, particularly affecting young women and migrant workers

Cotton dust in mill environments causes byssinosis, a chronic respiratory disease still common where ventilation is inadequate

Cotton uses a disproportionate share of global pesticides relative to the land it occupies, with documented health effects on farmers and farming communities

Environmental

Cotton is one of the most water-intensive crops in textiles. The drying of the Aral Sea, drained largely by Soviet-era irrigation programmes, is the most-cited example of long-term ecological damage

Pesticide and fertiliser run-off contributes to soil degradation and freshwater contamination in cultivation regions

Conventional dyeing and finishing of cotton fabric is chemically intensive and a major source of wastewater pollution where treatment infrastructure is weak

Key certifications and audits

GOTS (Global Organic Textile Standard). Covers organic cotton from harvest through finished garment. Requires a minimum of 70% organic fibre, with ecological and social criteria audited at every processing stage. The strongest scheme on cotton.

OCS (Organic Content Standard). Verifies organic content along the supply chain. Covers material identity but not processing conditions or labour, so lighter than GOTS.

Better Cotton. The largest cotton sustainability programme by volume (around 23% of global cotton). Trains farmers in better practices but operates on mass balance, meaning the physical cotton in a "Better Cotton" garment is not necessarily grown to its standards.

Fairtrade Cotton. Focuses on smallholder farmer income, with guaranteed minimum prices and a premium. Prohibits child labour and GM seed. Smaller volumes; mostly West African origin.

OEKO-TEX STANDARD 100. Tests finished fabric for harmful chemical residues. Product-level chemistry only; says nothing about how the fabric was produced.

Price

Cotton shirting wholesales at USD 4 to 9 per linear metre, driven by yarn count, staple length, certification, and origin. Organic cotton fabric runs 25 to 40% above conventional.

-

% of global fibre: Under 1%

Production countries: France (around 60% of global flax fibre), Belgium, Netherlands. Most fibre is then spun in China.

Benefits

A bast fibre made from the flax plant, with a crisp hand that softens with washing.

Naturally cool, breathable, and antibacterial.

One of the longest-lasting natural fibres.

Cultivated in Europe with no irrigation in normal years and minimal chemical inputs.

Premium retail position supports stronger margins.

Risks

Human & health

The European farm stage is widely considered low-risk on labour and environmental grounds, sitting under the European Flax charter

Most European-grown flax is shipped to China for spinning, where labour conditions, working hours, and chemical management vary widely and are rarely disclosed in brand-facing documentation

Dyeing and finishing of linen fabric carries the same chemical exposure risks for workers as cotton or viscose dyehouses

Environmental

Cultivation footprint is significantly lower than cotton: rainfed, no GMOs, low fertiliser use

Wastewater from dyeing and finishing remains a concern wherever the fabric is processed

Flax fibre prices are volatile, fluctuating significantly between harvests, which creates supply-side risk for seasonal programmes

Key certifications and audits

Masters of FLAX FIBRE™ (formerly European Flax™). Guarantees European origin and field-to-scutch documentation, audited by Bureau Veritas. Covers cultivation only.

Masters of LINEN™. Adds European spinning and weaving on top of Masters of FLAX FIBRE™. Closes the most opaque part of the linen supply chain.

GOTS. Applicable to organic linen, though volumes remain small.

OEKO-TEX STANDARD 100. Finished-fabric chemistry testing for harmful residues.

ZDHC (Zero Discharge of Hazardous Chemicals). Wastewater and chemical management standards applied at the dyehouse stage.

Price

European linen fabric wholesales at €11 to 22 per linear metre at 150 cm width for mid-weight qualities. Chinese-spun linen runs USD 2 to 5 per linear metre.

-

% of global fibre: Around 0.9%, approximately 1 million tonnes per year

Production countries: Australia (around 70% of merino used in apparel), China, New Zealand, the United Kingdom, Turkey, South Africa

Benefits

A keratin fibre with natural crimp that gives loft and warmth.

Insulates when wet, regulates humidity, resists odour, takes dye well.

One of the more traceable natural fibres because the animal retains a clear geographic origin.

Strong premium positioning and durable garments.

Risks

Human & health

Mill-stage risks in wool are relatively well-regulated compared with cotton or viscose

Smallholder farmers in remote grazing regions face exposure to volatile raw wool prices and concentrated buyer power, which affects income stability

Animal welfare

Mulesing, the surgical removal of skin around a sheep's rear to prevent flystrike, remains common in Australia despite alternatives. New Zealand banned the practice in 2018

Live sheep export by sea has been a documented source of significant welfare problems. Australia has legislated to end the practice from 1 May 2028

Environmental

Wool has a high greenhouse gas footprint per kg, driven mostly by enteric methane from sheep

Land use is significant in major producing countries, with debates over conversion of native grasslands and grazing pressure on biodiversity

Key certifications and audits

RWS (Responsible Wool Standard). Full chain of custody plus animal welfare criteria based on the Five Freedoms. Prohibits mulesing. The most substantive wool certification.

ZQ Merino. New Zealand-specific. Non-mulesing, with animal welfare, environmental, and farmer fair-pricing criteria.

SustainaWOOL. Australian. Tiered scheme that includes mulesing disclosure rather than a ban.

Woolmark. Covers fibre content and quality only. Not a sustainability or welfare certification.

GOTS. Applies to organic wool, with ecological and social criteria. Smaller volumes.

Price

Finished merino fabric wholesales at GBP 30 to 90 per linear metre, depending on micron, mill, and blend.

-

% of global fibre: Under 0.1%

Production countries: China (54%), India (14%), with Uzbekistan and Brazil the other meaningful producers

Benefits

A continuous protein filament fibre, exceptionally strong for its weight.

Natural sheen, and a drape no other fibre matches.

Heritage value supports premium pricing.

Takes dye with deep saturation.

Risks

Human & health

Silk reeling involves dipping cocoons into hot water, with documented burns, infections, and respiratory issues among workers

Bonded and child labour have been documented in Indian silk reeling for decades. The US Department of Labor still lists Indian silk fabric and silk thread as goods produced by child or forced labour

The reeling stage is among the lowest-paid and least-regulated parts of the silk supply chain

Animal

Conventional silk production kills silkworms inside their cocoons, by steaming or boiling, in order to preserve filament length. Volumes are very large at industry scale

Environmental

Mulberry cultivation is land- and water-intensive, particularly in dry regions

Chemical use in degumming and dyeing carries the usual wastewater profile of textile finishing

Key certifications and audits

OEKO-TEX STANDARD 100. Finished-fabric chemistry testing. The most common silk certification, but it covers chemistry only.

OEKO-TEX STeP. Site-level audit of production facilities: chemistry, environmental management, social compliance, occupational health and safety.

GOTS. Possible for organic silk but rare in practice. Where available, it covers the strongest set of criteria for the fibre.

Peace silk / Ahimsa silk. A marketing claim, not a certification. Asserts that worms are allowed to emerge before reeling, but is not independently audited at scale.

No widely adopted farm-to-finished chain-of-custody scheme currently exists for mulberry silk.

Price

Mulberry silk charmeuse wholesales at USD 11 to 40 per linear metre, depending on momme and grade. Heavy 30 to 40 momme silk reaches USD 60 to 110 per linear metre at the high end.

Cellulosic

-

% of global fibre: Around 5%

Production countries: China (over 65% of global supply), India (Aditya Birla / Grasim Industries), Indonesia (Asia Pacific Rayon and Indo Bharat Rayon), Austria (Lenzing)

Benefits

Made from dissolved wood pulp, with a soft drape and silk-like hand.

Takes colour cleanly and blends well with most other fibres.

Available at high volume and short lead times.

Significantly cheaper than silk for similar visual effect.

Risks

The central risk in viscose is the chemistry used to turn wood pulp into fibre. The conventional process relies on carbon disulphide (CS2), a hazardous solvent, and a sulphuric acid bath.

Human & health

CS2 exposure has been linked to elevated rates of cardiovascular disease, neurological damage, and reproductive problems among workers in long-running cohort studies

Pollution incidents at viscose plants have been documented in India and Indonesia, in some cases affecting communities living downstream from the facility

Worker health protections vary widely between producers

Environmental

Conventional viscose production generates significant air and water pollution where facilities lack closed-loop chemical recovery

Wood pulp sourcing carries forest-conversion risk, which Canopy's Hot Button Report tracks across most of global capacity

Wastewater from viscose facilities has been linked to severe river pollution at multiple sites

Key certifications and audits

Canopy Hot Button. Annual ranking of viscose and lyocell producers on forest-sourcing risk, with a colour-coded shirt rating. "Dark green" indicates lowest risk.

FSC (Forest Stewardship Council). Chain-of-custody certification for sustainably managed forests, applied at the pulp input stage.

PEFC (Programme for the Endorsement of Forest Certification). Alternative forest-certification scheme, often more locally administered than FSC.

ZDHC MMCF Guidelines. Facility-level standard for chemical and wastewater management at manmade cellulosic producers.

EU Ecolabel. Voluntary EU-administered standard covering lifecycle environmental criteria. Available for some viscose products.

Price

Ex-China viscose wholesales at USD 0.60 to 1.20 per linear metre. European-finished or blended viscose runs €6 to 11 per linear metre.

-

% of global fibre: Under 1%, around 360,000 tonnes of TENCEL™ Lyocell produced globally in 2023

Production countries: Lenzing's plants in Austria, the Czech Republic, Thailand, the United Kingdom, the United States, and China

Benefits

Made from dissolved wood pulp like viscose, but using a different solvent (NMMO).

Recovers around 99.8% of the solvent in a closed loop, removing most of the worker health risks associated with CS2.

Soft hand, strong wet performance, drape close to silk.

Lower chemical footprint than conventional viscose at production stage.

Risks

Human & health

The closed-loop NMMO process removes most of the chemical exposure problem that defines viscose

Generic lyocell from non-Lenzing producers may not run the same closed-loop recovery, and can approach viscose's chemical profile

Environmental

Forest sourcing remains a relevant risk, mitigated by FSC, PEFC, and Canopy's tracking

Energy demand at Lenzing plants is significant, though closed-loop chemistry removes most of viscose's wastewater problem

Key certifications and audits

TENCEL™ and VEOCEL™. Lenzing-owned trademarks that identify Lenzing-produced lyocell, made with the closed-loop NMMO process and distinct from generic lyocell. Includes molecular fibre markers for identification through finishing.

EU Ecolabel. Applies to TENCEL™ Lyocell products. Covers lifecycle environmental criteria.

FSC and PEFC. Pulp-input level certification.

Canopy Hot Button. Lenzing has held the highest ("dark green") ranking in recent years.

OEKO-TEX STANDARD 100. Finished-fabric chemistry testing.

Price

TENCEL™ lyocell fabric wholesales at €10 to 17 per linear metre at 150 cm width for basic twills, shirting, and crepes. Heavier TENCEL/linen blends run €18 to 28 per linear metre.

Synthetic

-

% of global fibre: 59%, 78 million tonnes in 2024, 88% of it fossil-based

Production countries: China (over 70% of global capacity), India (Reliance, Indorama), Taiwan, South Korea

Benefits

A plastic fibre made from crude-oil-derived chemicals (polyethylene terephthalate, or PET).

Cheap, durable, wrinkle-resistant, quick-drying.

Dye-stable at scale, with consistent results across batches.

Available at short lead times from mills running year-round, with no agricultural cycle.

Risks

Human & health

Petrochemical workers face exposure to benzene, toluene, and volatile organic compounds at refinery and polymerisation stages, which is rarely audited by the fashion industry

Polyester microfibres have been found in drinking water, food, human blood, and Arctic sediment, with persistence on century timescales

Worker conditions in synthetic mills tend to be better regulated than in cotton spinning, but vary by country

Environmental

Polyester production is fossil-fuel based and represents one of the largest carbon footprints across the textile sector by total volume

Garments shed substantial quantities of microplastic fibres during washing, with research consistently documenting hundreds of thousands of fibres released per wash load

Wear alone, without washing, also releases significant fibre quantities into the air

Key certifications and audits

OEKO-TEX STANDARD 100. Finished-fabric chemistry testing.

Bluesign®. System covering chemicals, water, energy, emissions, and occupational health at the manufacturing stage. Audits chemical inputs as well as processes.

ZDHC MRSL (Manufacturing Restricted Substances List). Bans or restricts intentional use of hazardous chemicals across the supply chain.

There is no equivalent of cotton or wool farm-level traceability for polyester. Once polymerisation occurs, feedstock origin cannot be determined from the fibre.

Price

Woven polyester fabric from China wholesales at USD 0.60 to 2.00 per linear metre. Premium functional polyester reaches USD 4 to 6 per linear metre.

-

% of global fibre: 12% of total polyester output, 9.3 million tonnes in 2024. Share declined from 12.5% the previous year because virgin polyester grew faster.

Production countries: China, Taiwan, Vietnam dominate. 98% of rPET still comes from post-consumer PET bottles, not from textile waste.

Benefits

Same technical performance as virgin polyester at the fibre level.

Lower upstream carbon footprint per kg than virgin polyester.

Supports brand and procurement targets for recycled content.

RisksA December 2025 laboratory study by the Microplastic Research Group at Cukurova University, commissioned by the Changing Markets Foundation, tested 23 virgin and recycled polyester items from major brands and reframed several common assumptions about rPET.

Human & health

Recycled polyester fibres tested were on average around 20% smaller than virgin fibres, which makes them more mobile in the environment and more likely to enter biological systems

Worker conditions at sorting and recycling facilities, especially in informal recycling chains, are rarely audited

Environmental

Recycled polyester released significantly more microfibres than virgin polyester in controlled testing (around 55% more on average), with wide variation between brands

Most recycled polyester is made from PET bottles, which can otherwise be recycled indefinitely as food-grade material. Diverting them into textiles is a one-way move; the resulting fibre cannot practically be recycled again

Mechanically recycled polyester sheds further microfibres in subsequent recycling cycles

Key certifications and audits

GRS (Global Recycled Standard). Full-product chain of custody with a 20% recycled minimum (50% for consumer-facing labels), plus social and environmental criteria. The most substantive recycled-content scheme.

RCS (Recycled Claim Standard). Chain of custody only, with a 5% minimum and no environmental or social criteria.

OEKO-TEX STANDARD 100. Finished-fabric chemistry testing.

Price

GRS-certified recycled polyester fabric wholesales at USD 1.50 to 3.50 per linear metre.

Why this matters now

There are no "good" or "bad" fibres in absolute terms. Every fibre carries trade-offs, and choosing the right one depends on the product, its use, and what evidence is available about its supply chain.

What is changing is the legal context. From 27 September 2026, the EU's Empowering Consumers for the Green Transition Directive will ban generic environmental claims ("sustainable", "eco-friendly", "climate neutral") on products sold to EU consumers unless backed by recognised certification. From mid-2028, Digital Product Passports become mandatory for all new textile products on the EU market, requiring fibre composition, chemistry, water use, worker welfare, and end-of-life data to travel with the product. Both apply to UK brands selling into the EU regardless of where the brand is headquartered.

For a fuller breakdown of the EU green claims rules and how to prepare, see Article 001.

How to reduce the risks when sourcing

Certifications are useful, but they do not solve everything on their own. The most reliable approach is to build relationships with suppliers, understand what evidence they can actually provide, and identify where their visibility ends. The starting point for each fibre:

Cotton. Farm declaration at bale level, spinning-mill location, and GOTS or Better Cotton chain-of-custody transaction certificates. For Chinese cotton, a written Xinjiang sourcing statement and documentary evidence of non-Xinjiang ginning.

Linen. Masters of FLAX FIBRE™ and Masters of LINEN™ certificates rather than "European flax" used as marketing language. If spinning is in China, OEKO-TEX STANDARD 100 and ZDHC dye-house data.

Wool. RWS scope and transaction certificates, mulesing status with pain relief documentation, and country of origin at the farm rather than the shearing shed.

Silk. Reeling location, hot-water practice, worker age documents, and OEKO-TEX STeP at the reeling site. If a supplier cannot provide these, that absence is itself useful information.

Viscose. Canopy Hot Button rating of the producer (green-shirt minimum), ZDHC MMCF assessment reports, and FSC or PEFC pulp certificates.

Tencel. Specify Lenzing TENCEL™ or VEOCEL™ with molecular marker documentation. Generic lyocell does not carry the same guarantee.

Polyester. Bluesign®, OEKO-TEX STANDARD 100, and mill-level microfibre shedding data if the product is washable.

Recycled polyester. A GRS transaction certificate matching the specific order, not the mill's general scope certificate.

Behind every fibre label there is a chain of decisions, and behind every chain there are people. Keeping them visible is becoming both an ethical position and, increasingly, a legal requirement.

Key sources

Textile Exchange, Materials Market Report 2025, September 2025. https://textileexchange.org/knowledge-center/reports/materials-market-report-2025/

US Department of Labor, 2024 List of Goods Produced by Child Labor or Forced Labor. https://www.dol.gov/agencies/ilab/reports/child-labor/list-of-goods-print

Changing Markets Foundation, Spinning Greenwash, December 2025. https://changingmarkets.org/report/spinning-greenwash/

t.issu & co connects mid-size EU and UK fashion brands with pre-qualified Indian textile mills, with chain-of-custody documentation structured before orders arrive, priced into the contract, and tied to specific mills rather than brand-level claims. Get in touch.